MANUAL OF FINANCIAL MANAGEMENT AND LEGAL REGULATIONS

Item

- Title

-

MANUAL OF FINANCIAL

MANAGEMENT AND LEGAL

REGULATIONS - extracted text

-

Manual of Financial

Management and Legal

Regulations

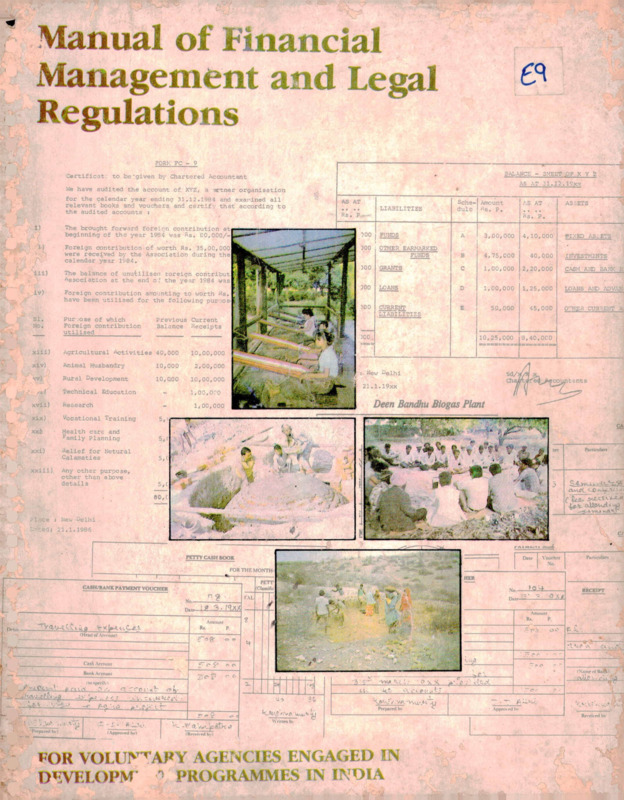

FORM FC - 9

Certificat

BALANCE - SWEET .OF X Y 2

to be'given by Chartered Accountant

AS AT 31.12.19x.x

We have audited the account of XYZ, a wtner organisation

for the calendar year ending 31.12.1984 and examined all

relevant books and vouchers and certify that according to

the audited accounts i

AS AT

The brought forward foreign contribution ati

beginning of the year 1984 toas Rs. SO,000/-

I)

Foreign contribution of worth Rs. 35,00,000

were received by the Association during the

calendar year 1984.

ill)

The balance of unutilised toreign contribut

Association at the end o: the year 1984 was

iv)

Foreign contribution amounting to worth Rs.

have been utilised for the following puruOsi

Purpose of which

Foreign contribution

utilised

/ -

w

1®'

r’ r-Cr-v....

Previous Current

Balance Receipts

I

e,

w-

:■

Agricultural Activities 40,000

10,00,000

xiv)

Animal Husbandry

10,000

2,00,000

?00

FUNDS

A

3,00,000

4,10,000

>00

OTHER EARMARKED

FUNDS

B

4,75,000

40,000

500

GRANTS

C

1,00,000

2,20,000

CASH AND BANK £

100

LOANS

D

1,00,000

1,25,000

LOANS AND .'&V&

)00

CURRENT

LIABILITIES

50,000

45,000

O^Hpp. CURRENT

10,25,000

9,40,000

)00

Rural Development

10,000

10,00,000

Technical Education

1,00,000

xvii)

Research

1,00,000

xix)

Vocational Training

XX&

J

C7X

I1-/

. New °elhi

I

21.1.19xx

Deen Bandhu Biogas Plant

5,(

~~1

■■

■.

■

-

#

Pnrcirulan

.<4

5,<

Any other purpose,

other than above

details

CA

■

■

M

-

’

xxiii)

INVESTMENTS

'<

'

Relief for Netural

Calamaties

xxi)

■FIXED AScETS

e==:BSS3S=i

5,<;

• Health care and

family Planning

ASSETS

Rs. P.

s?

Xiii)

AS AT

Sche Amount

dule Rs. P.

LIABILITIES

Rs. P,

•>

I

5,(

~

O'’

<-0 kUjv ■- x-

80, C

.JXiXS'.iMLX

■’ -,

: New Delhi

: 21.1.1986

I

]

Cf

rniMiuni oamw

PETTY CASH BOOK

CASH/BANK PAYMENT VOUCHER

No.-

—12—

Datr-

15> .3 •

Dair

I

i or

PETTE

_ kaaMificfe

CAlJ

■

HER

* J-

-

Debit

RECEIPT

No.Dair

•«!

'’A

Amount

JU.

I

Amount

Hi.

Paniculan

Voucher

No.

n£

p.

(Head of Account)

H

"1

Cash Account

(Name of BamU

Bank Aecnunt

' *• .■

.

,

(tnipefilv)

V <!

p'. £> ■;

■-

'X-'

.•■ V'. r c iAi^'4\ :

:—^-tr

* -i:(Approved by)

IC

t<;..

[

d.^cX.

*•'<<<-pt'

5^

I

Prepared bv

Apptm-cd hv

Rcreivcd bv

Written by

(Received by)

» ()R VOLU^ARY AGENCIES ENGAGED IN

PROGRAMMES IN INDIA

DHVELOPM

MANUAL OF FINANCIAL

MANAGEMENT AND LEGAL

REGULATIONS

FOR VOLUNTARY AGENCIES ENGAGED IN

DEVELOPMENT PROGRAMMES IN INDIA

THAKUR, VAIDYANATH AIYAR & CO.

212, DEEN DAYAL MARG,

NEW DELHI

INDIA

X

-

All rights reserved. Mo part of this manual

mav be reproduced in any form, without permission

in writing from the publishers.

January. J986

PubKshed by Shri K.N. Gupta on behalf of

Thakur. Vaidyanath Aiyar & Co.

212. Deen Dayal Marg. New Delhi—110 002

Printed by N.K. Enterprises. 4782/2-23 Darya Ganj. New Delhi-110 002.

fr

Preface

I his Manual has been prepared with a view to providing general and specific guidelines to the

voluntary agencies engaged in development programmes in India. It purports to fill the gap

hitherto existing in recording and reporting of their operations which is so very necessary for

accomplishing their basic objectives. The Manual seeks to give a detailed description of

logistics, policy matters and mechanics as an aid in the preparation of budgets alongwith simple

and comprehensive system design for book-keeping and accounting functions. The utilisation of

resources and the ensuing flow of information for managerial planning and control have also

been presented in an easy to follow format. Special emphasis has been accorded to reporting

systems for general as well as special funds to highlight the growing quest for adequate

accountability. In addition, the legal regulations and their specific implications for accounting

and overall financial management have been clearly brought out. Detailed guidelines for

auditor s selection and the audit norms to be adopted by the project’s auditors have been

meaningfully explained, thus strengthening the overall accountability expected of these

agencies.

Shri K.N. Gupta, the principal partner of the firm who was concerned with the preparation of

this Manual, had spent considerable time in visiting the various voluntary organisations in

India and having discussions with them as well as Funding agencies in countries like West

Germany, Holland, U.K. and Switzerland.

We would like to express our grateful thanks to late Professor T.S. Grewal, formerly Director,

Board of Studies, The Institute of Chartered Accountants of India, New Delhi for going

through the first draft and offering valuablcsuggestions.

We would like to express our indebtedness to Dr. Hartmut Bauer and Dr. Badal Sen Gupta of

EZE, West Germany for their dynamic initiative and providing underlying meanings to

concepts and nauances used in the Manual.

We would, however, welcome any suggestions from the partner organisations so as to enable us

to improve the contents of the manual for the next edition.

January. 1986.

New Delhi

THAKUR, VAIDYANATH AIYAR & CO.

♦

Foreword

The voluntary organisations have a fine record of dedicated, committed and selfless service for

the benefit of poor, deprived and needy people. Their proximity to and complete identification

with the people they work with is another attribute of voluntary organisations that makes them

distinctively superior to organisations working in impersonal and routine manner.

However the funds received by voluntary organisations, and the manner in which it is received,

the way it is utilised, the system of account keeping they follow, the reporting they do. the extent

to which they follow the laws of the land and administrative rules enforced by authorities from

time to time, are the weak points of most, if not all of them.

In recent years efforts have been made by various organisations to improve their financial

accountability through training programmes, seminars, conferences, etc., on simple account

ing and book-keeping and through detailed circulars on requirements of Income Tax Act,

Foreign Contribution Regulation Act and other important legal provisions. Through these

attempts, the accountability and transparency of voluntary organisations has improved. The

present publication “Manual of Financial Management and Legal Regulations—For Volun

tary Agencies engaged in Development Programmes in India” prepared by M/s Thakur,

Vaidyanath Aiyar & Co. (TVA), New Delhi, a firm of Chartered Accountants of long standing

is another step forward in this direction.

This publication is the result of a long process of preparation of the text, updating the

information, consultation with major partners and field testing with user organisations scat

tered in remote villages. This process would not have been completed but for the active

participation of Dr. Hartmut Bauer, Director, EZE, West Germany and Shri K.N. Gupta,

partner. TVA. New Delhi.

We hope that voluntary organisations will receive this publication with enthusiasm and use it

for further improvement in their accountability.

January, 1986

New Delhi

Major J.K. Michael

Director

Church’s Auxiliary For Social Action

J.B. Singh

Executive Director

Action For Food Production

CONTENTS

CHAPTER

I

II

III

IV

V

VI

VII

VIII

IX

Page

Introduction

Budget of Project/Programme

Project/Programme Implementation and Transfer of Funds by

Funding Agencies

Book-keeping System

Special Funds

Reporting

Legal Regulations in India

Guidance Note on the Selection of An Auditor

Audit Guidelines

19

26

78

103

112

160

163

ANNEXURES

Information on Funding Agencies:

‘A’ Evangelische Zentralstella Fur Entwicklungshilfe E.V. (EZE)

(i) Agreement Between EZE and Project Partner

(ii) Forms and Explanatory Notes

Abbreviations Used

Index

189

194

212

213

1

4

MANUAL OF FINANCIAL MANAGEMENT

AND

LEGAL REGULATIONS

I

INTRODUCTION

CHAPTER I

Introduction

Page

Accounting is a must

Obligations of Funding Agencies

Need of a Manual

Role of Auditors

1

1

2

3

1.

Introduction

Accounting is a must

1.01

Accounting is a necessary part of economic man. This is true of today as it was in ancient

times. While the sophistication of accounting will change in response to the complexity of

the social and economic systems it serves, some level of accounting appears essential in

every social order.

1.02

Accounting is the discipline which provides financial and other information essential to

the efficient conduct and evaluation of the activities of any organisation.

1.03

Accounting is the tool for a proper financial management. The importance of financial

management cannot be over-emphasised. Sound financial management is essential in all

organisations—profit or non-profit—where funds are involved. It attempts to use the

funds in the most productive manner.

Obligations of Funding Agencies

1.04

International Funding Agencies have been assisting the developing countries in carrying

out projects and programmes which—

— give primary attention to the poorest groups in society

— provide the active participation of the people involved

— help to create and strengthen people’s self-relience

1.05

The funding agencies are collecting funds from the people in their countries and are,

therefore, themselves under public observation and control and owe a. responsibility to

the ultimate provider of funds. On the one side, this encounters difficulties because the

accountability of funds is subject to the strict rules of the Public Budget Regulations. On

the other side, it offers the great possibility that the engagement of the non-governmental

organisations for the poor in the world can be made clear. For this purpose the funding

agencies are to furnish proof to the public concerned of the economical and successful

utilisation of the money given in Trust.

1.06

Broadly the International Funding Agencies are accountable for:

— the careful choice of the partner organisations in the developing countries and to agree

on clear rules of co-operation—the partner organisations being responsible for the

planning and implementation of the projects and programmes;

— funds being used for the purposes for which it is agreed upon and that they are used

efficiently and economically;

— the accounting systems used by the project organisations to be transparent, clearly

showing in which way funds have been spent;

— ensuring that project organisations, in the interest of accountability submit progress

reports and duly audited (by independent auditors) financial statements.

1.07

The Funding Agencies have certain constraints in enic icmg me accountability by the

persons in charge of the management of the projects. The first constraint is one of moral

attitude—instead of policing, an attitude of partnership and self-discipline is adopted.

The funding agencies normally are not allowed, in order to optimise the use of funds for

the developmental needs, a large budget by way of overheads to oversee and administer

the disbursement of funds and supervision of the project that they are proceeding as

planned. This deficiency is easily remedied by properly assisting and guiding the persons

in charge of the project in their task of accountability.

Need of a Manual

1.08

It is in this context that TVA has—jointly with EZE—carried out a workshop in Delhi in

January 1985. 34 experienced representatives from partner organisations and auditors

attended this workshop with the aim of discussing the draft of a manual for “Financial

Management and Legal Regulations for Voluntary Agencies” engaged in the field of

development programmes. This manual is seen as a helping instrument for those

connected with the project management. It would serve as a practical guide on matters

connected with project management such as:

— preparation of the budget for the project/programme,

— procedure for transfer of funds by funding agencies for project/programme

implementation.

— minimum books of account and other related records that are to be maintained.

— a simple accounting system to meet the needs of management information and

establish accountability,

— the meaning and operation of special funds,

— the preparation of financial statements and progress reports,

— the implications of the legal scenario (as it obtains in India) in which the project

organisations are likely to operate, etc..

1.09

In this manual, an attempt has been made to explain in simple, precise and lucid terms

but in sufficient and appropriate details all aspects that a project manager as well as those

in charge of actually executing the project are familiar and thorough with the systems

and procedures.

1.10

It is hoped this manual would serve as a tool for effectively discharging the responsibility

of accountability by the partners of the project organisation to the funding agencies

which in turn would help the latter in complying with their trust duties to the govern

ment and public concerned.

1.11

It is the aim of this manual to improve i^pon the financial accountability oi the project

the Govt, of India and last

partners towards the beneficiaries, their own constituency,

<

but not least the overseas funding agencies.

1.12

This manual is in the first instance meant for EZE partners. It could, however, also be of

assistance to other organisations which work together with other funding agencies since

most of the chapters in this manual are applicable to international relations.

2

Role of Auditors

1.13

The other tool for achieving the objective of ensuring compliai

. mce with accountablity is

the examination of the records by independent auditors and their certificate that the

funds have been utilised properly, efficiently and economically. Such an independent

examination and certification lends credence to the financial statements and enhances

their reliability.

1.14

This independent certificate is provided by the members of the recognised Accounting

Bodies of the country where the projects are executed and whose members by law are the

only competent professionals who could carry out such audits. In the practice of public

accounting, such members bring competence of professional quality, independence and

a strong concern for the usefulness of their report. The professional quality of their service

is based on the requirements for the admission to such membership—the education,

experience, examination, the ethical and technical standards established and enforced

by their professional bodies.

1.15

The examination of the financial statements requires the professional accountants to

review many aspects of an organisation’s activities and procedures. Consequently, they

can advise on needed improvements in internalcontrol and give constructive suggestions

on financial, tax and other operating matters.

1.16 As a support measure to the functions of the indepenucnt auditors, an audit manual

entitled General Guidelines for Audit” has been prepared. This audit manual sets out

in clear detail how the independent auditor could go about the task of conducting the

audit of non-profit public cause serving projects. Here again, an attempt has been made

to lay bare the objective behind each of the examination/enquiry of the auditor which

must necessarily be made before the auditor forms his opinion on several matters on

which he is called upon to report. A perusal of these guidelines even by the project

managers would enlighten them about the rational of the approach by the auditors and

thus remove any misgivings which might otherwise arise.

3

MANUAL OF FINANCIAL MANAGEMENT

AND

LEGAL REGULATIONS

II BUDGET OF PROJECT/PROGRAMME

CHAPTER II

Budget Of Project/Programme

Page

Introduction

Preparation of Budget

Cost Plan

Finance Plan

Use of own Means for Financing Projects/Programmes

Contribution in Cash

Contribution in non-cash inputs

4

4

5

6

7

8

9

Forms

Item Structure of a Building Project

Item Structure of Establishment of Village Industries and Training Centres

Cost Plan—Programme Activities Budget

Administrative Expenses Budget for Programme co-ordination

Details of Staff Salary and Benefits

Finance Plan—Source of Funds

12

13

15

16

17

18

II

Budget Of Project/Programme

Introduction

2.01 A project is understood as an undertaking co serve a middle to long term purpose/objective

in which all the necessary investment is essentially of a capital nature. A programme is

understood as an undertaking which has a limited and specific target, a limited period of

implementation and a limited financial outlay, (please refer also to paragraph 2.16 of this

chapter).

2.02 Budget involves a system of planning, executing the plan and evaluating performance and

financial working of an organisation in which activities are planned in advance.

2.03 The philosophy behind the budget is that nothing would be allowed to occur in a

haphazard manner but there should be an objective towards which the organisation is to

progress in an orderly and pre-planned manner. In order to aid this process of planning, the

mechanism of a plan (which is the picture at a given point of time, the planning process would

lead to) is adopted. Thus the plan is the commitment to a set course of action required to realise

the results that are depicted in the plan. The planning process stipulates thinking at all levels of

management and serves as a measure of performance^

2.04 Hence the organisation should plan its activities in advance, carry out the plan and

institute appropriate techniques of observation and reporting to ensure that the deviations from

plan are properly analysed and handled.

2.05 In this system of control, performances are checked with the pre-planned figures and the

variances are analysed.

2.06 Hence, following are the important characteristics of a budget:

(a) It is a financial and/or quantitative statement;

(b) Prepared well in advance;

(c) For a definite period of time;

(d) For the attainment of objectives and measures agreed upon.

2.07 11 would therefore be advisable for every organisation to prepare a budget since this would

enable it to plan out the activities of the ensuing year/s. This also helps in planning the

commitments and to activate resource mobilisation to meet such commitments.

2.08 Institutions which receive foreign contribution from International Funding Agencies are

usually required to present a budget of programme activities for a specified period.

Preparation of Budget

2.09 The voluntary organisations dealing with funding agencies prepare a

4

—Cost plan

and

— Finance plan

to budget their activities for ensuing year/years in Foreign currency and in National

currency.

2.10 For the purpose of administrative control, the basis of calculation is normally taken as

three years for programmes and in respect of projects it varies according to its nature.

2.11 A ‘Cost Plan’ is a schedule of budgeted costs divided into two major parts, namely:

— ProgrammeActivities Budget

—Administrative Budget for Prqject/Programme Co-ordination.

2.12 A ‘Finance Plan’ is a schedule of budgeted sources of funds.

Cost Plan—Programme Activities Budget

2.13 This woulo include programmes/prqjects undertaken/to be undertaken by the organisa

tion for a specified period. This would include:

— Capital costs

— Programme costs

— Office costs

— Reserves

2.14 Detailed sub-schedules should be prepared for each of the sub-Heads.

2.15 Capital costs would represent expenditure of capital nature. For example:

— Construction of lift irrigation system including pipe systems and land development;

— Construction and equipping of a school building and teacher’s accommodation;

— Setting up a training and demonstration farm, land development, irrigation etc.

(. ..acres);

— Land development and sowing oil seeds;

— Construction of lift irrigation units (including canals/pipe systems).

2.16 A programme is understood as an undertaking which clearly spells out operational

targets, a specific time horizon and limited financial outlay. This could be:

— an adult education programme to make 10,000 Harijan women and men in 50 villages of

Nalgonda distt. in Andhra Pradesh State functionally literate within a time horizon of 3

years; or

— an immunization programme to immunize 10,000 children under 6 years in the same

villages against DPT (Disease) within 3 years.

2.17 A programme may include one specific target and the programme component to achieve it

or several targets and accordingly several programme components to achieve the same.

2.18 Programme costs would include:

5

— Office costs

— Capital costs (with limited utilisation)

— Reserves

2.19 These costs should be clearly related to and necessary for achieving the specified targets

within defined period of time. The overhead expenditure independent of specific programme of

an institution or organisation is not programme costs.

2.20 Office costs would normally include salary of the project staff which is directly involved in

the implementation of the project/programme.

2.21 Cost item “Reserves” is primarily meant to be utilised for:

(a) price increase in thejnain budget items not anticipated earlier (but accounted for under

respective cost items);

(b) Audit fee and expenses;

(c) Bank charges; and

(d) financing unforeseen measures for which prior approval of the funding agencies is to be

obtained.

Cost Plan—Administrative Expenses Budget (for project/pro

gramme Co-ordination)

2.22 This would include administrative expenses incurred for co-ordination of various pro

grammes i.e. staff salary and benefits (excluding project staff which is directly involved in

implementation of the project/programme); travel and conveyance; operating costs of vehicles,

rent, rates & taxes, water and electricity expenses; office up-keep; communications; meetings;

seminars; legal expenses etc..

2.23 Wherever needed, separate sub-schedule for details should be prepared, for example staff

salary and benefits.

2.24 A typical example of item structure of a cost plan (schedule of budgeted costs) in respect of

a building project versus other projects/programmes, say, establishment of village industries,

and village industries oriented training centres is given on page Nos. 12 to 14.

Finance Plan—Schedule of Budgeted Sources of Funds

2.25 A finance plan is a schedule of budgeted sources offunds for financing project/programme

related expenditure. The normal pattern of financing the Programme Activities Budget and

Administrative Budget (for project/programme co-ordination) is as under:

— Contribution by the Funding Agencies; and

— Contribution by the Project-Partner.

2.26 There are good reasons for the project-partner to participate in the expenditure (upto a

certain percentage) to be incurred on a programme/project. For example:

— strengthening of responsibility and decision making, as principles of co-operation;

— motivation of the beneficiaries to contribute to their project/programme;

— better co-operation between beneficiaries and credit institutions in case ofbank financing:

6

— educational effects for the beneficiaries; and

— creating conditions for the continuation of the project after contributions from funding

agencies have been exhausted.

2.27 Funding agencies are contributing a specified % to the actual expenditure but not more

than amount sanctioned in foreign currency. In cases of exchange variations or over-spending

of budget, the responsibility for financing such costs lies primarily with the project-partner.

There is however; a possibility for applying for additional funds which can be considered by the

funding agencies on case to case basis.

2.28 The project-partners are expected to utilise as high a portion of their budgeted financial

contribution as possible in the beginning of each project/programme. If this is not possible,

funding agencies would insist that expenditure is at least financed by the project partner

proportionate to his share in the schedule of budgeted sources of funds. In case of difficulties,

special arrangements can be made between the project partner and the funding agencies.

2.29 It shall however, be ensured that the contribution to be made by the funding agencies and

the project-partners should be finalised and agreed upon at an early date so that there is no

ambiguity at a later date.

2.30 Contribution to be made by the project-partner can be either in cash or in non-cash

inputs.

2.31 It would be advisable if the project-partner is in a position to assess separately the

quantum of its contribution in cash and non-cash inputs in the beginning itself. Further, the

composition of non-cash inputs may be in the form of donations of land, building, capital

equipments, labour, material and other services.

2.32 It would be advisable if non-cash contribution in various identifiable forms are estimated

by the project-partner at the time of working out the source of funds for financing a particular

project/programme so that there is no room for difference of opinion between the funding

agencies and the project-partner at a' later stage.

2.33 A set of budget formats is given on page Nos. 15 to 18.

2.34 The budget estimates prepared initially for a specified period for each programme/project

should be further split into monthly/quarterly/half-yearly targets so that actual results could be

compared with budgeted figures and timely corrective action is taken for achieving the planned

measures and objectives.

Use of “Own Means” for Financing Projects/Programmes

2.35 As explained in paras above, contribution by project-partner which is termed as “Own

Means” can be in cash or in non-cash inputs.

2.36 Cash and non-cash contributions can be ‘within’ and ‘outside’ finance plan. Cash and

non-cash contributions are treated ‘within’ finance plan, if they can be recorded in the books of

account of the partner organisation. Otherwise, they have to be estimated and reported

‘outside’ or separate from the budget and the financial statement e.g. if contribution to the

programme comes from third parties directly to the beneficiaries.

7

2.37 Cash and Non-cash contributions within Finance Plan: These could be as under:

‘Cash’contribution within Finance Plan:

— Own cash contribution by project partner

— Grant from other Funding Agencies

— Subsidy from State/Central Govt.

— Loans from banks (provided re-payment of loan is arranged independently)

Non-cash contribution within Finance Plan:

— If such non-cash inputs relate to the project e.g. it represents one of the items of the

approved budgeted costs—cost plan

— If such inputs can be easily evaluated and recorded in monetary terms in books ofaccount

— Cash and non-cash contributions within “Finance Plan” should be reflected in the

“financial statement” to be submitted to the funding agencies.

2.38 Cash and Non-cash contributions outside Finance Plan. These could be as under:

Cash contribution outside “Finance Plan ”

— Loans granted by banks directly to beneficiaries

Non-cash contribution outside “Finance Plan”

— Other services/materials provided by third parties directly to the beneficiaries (target

group)

2.39 Cash and Non-cash contributions outside finance plan should be reflected as an annexure

to the “financial statement” to be submitted to the funding agencies and explained adquately in

the progress reports.

2.40 The concept of “Own Means” can be clearly understood with the help of a chart given on

page No. 9.

Contribution in Cash

2.41 Contribution in cash can take the form of partner’s cash, donations in cash, membership

and other fees of the beneficiaries, loans from banks, subsidy/grant from Central/State Govt,

and funds for co-financing received from other funding agencies.

2.42 Donations: Donations received in cash (including cheques/money-orders/postal orders

etc.) by project-partner for implementing a project/programme shall be accounted for on the

receipt side of “Cash Book” on the basis of receipts issued to the donors.

2.43 It shall be ensured by the project-partner that all contributions received in cash/by

cheques/money-orders/postal orders etc. are promptly deposited intact into separately de

signated bank account of the project.

2.44 Loans from Bank: As a part of “Own Means” of financing, the pro ject-partner can obtain

8

OWN MEANS

CASH

i

z

X

I

z

NON-CASH

(a) Own cash

contribution by

Project-partner.

(a) Non-cash inputs:

i) Ifsuch rion-cash

inputs relate to

the project.

(b) Other Sources:

— Grant from other

funding agencies.

— Subsidy from Govt

— Loan from Banks.

ii) Such inputs can be

easily evaluated and

recorded in monetary

terms in books of account.

(c) —Cash income from fees

for attending Seminars/

Training Courses.

u:

C

I

Loans granted by Banks

directly to target population

(beneficiaries)

(a) Other services/materials

provided by third parties

directly to target population

group.

loans from bank for implementing the project/programme. It shall, however, be ensured that

the project/its beneficiaries are in a position to repay the bank loan independently.

2.45 It shall however, be ensured by the project-partner that no part of the land, building and

movable assets are pledged/hypothecated or charged with the bank without prior consultation

and consent of the funding agencies if the grant has been involved.

2.46 Subsidy/Grant from Central/State Govt.: If the capital costs forming part of an approved ‘cost

plan’ of a project/programme is eligible for subsidy/grant from Central/State Government, the

amount of subsidy/grant so received can be treated as a part of “Own Means” of financing by

the project-partner.

2.47 1 he amount of subsidy/grant received by means of a cheque/pay order shall be promptly

deposited into the designated bank account opened for the project and entered on the receipt

side of cash book.

Contribution in Non-Cash Inputs:

2.48 As explained earlier, contribution in non-cash inputs can be in the form of donations of

land, building, capital equipments, labour, materials and other services.

2.49 Before making commitment of an expenditure (either of a capital or revenue nature) to be

financed by funding agencies/own means, it shall be ensured by the project-partner that the

proposed expenditure forms part of the approved “Cost Plan”. If not. the ways and means of

financing the same should be explored outside the project. If the project-partner is not able to

arrange outside finance, consent of the funding agency should be taken in advance and in

exceptional cases well before the accounts are submitted for audit.

9

2.50 Particular care should be taken in making out vouchers in support of expenditure

representing the project-partner’s own non-cash contribution to ensure that they explain

adequately and in sufficient detail the nature and make up of such expenditure.

2.51 Donation of Land and/or Building: Donation of land and/or building made to a project/

programme can be accounted for as “Own Means” by the project-partner if the same forms

part of the approved “Cost Plan”. For this purpose, the following criteria should be adopted:

Land

— The acquisition of land should be budgeted in the approved “Cost Plan”;

— Total area of land;

— Prevalent market rate per acre/hectare;

— Cost of registration of land;

— Legal title to the property;

— Physical possession of the property;

— Acknowledgement from the donor; and

— Registration of land in favour of the organisation.

Building

— Construction/acquisition of building should be included in the approaved “Cost Plan ;

— Total covered area;

— Type of construction;

— PWD rate of construction per sq. ft.;

— Prevalent market rate as per certificate of architect/approved Civil Engineer;

— Legal title to the property;

— Acknowledgement from the donor;

— Physical possession of the property; and

— Registration of building in favour of the organisation.

2.52 Donation of Capital Equipments: There may be cases where the Farmers/Inhabitants/beneficiaries of a particular area may donate capital equipments for a project/programme (tractor,

vehicle etc.)

2.53 It shall, however, be ensured that:

. (a) capital equipments financed out of funds provided earlier are not charged to the project

again.

(b) In case of second hand capital equipments, they are not more than two years old.

2.54 The following points shall be taken into account while arriving at the value of the capital

equipments donated to the project:

— Nature of the capital equipment;

— Acquisition of capital equipment should be budgeted in the approved “Cost Plan ;

— Present condition of the equipment;

— Estimated realisable value, if sold in the market;

— Legal title to the property;

— Physical possession of the property;

— Acknowledgement from the donor; and

— Transfer of name in the vehicle registration book.

10

2.55 Donation of Labour: In a Project Implementation Programme, ‘Shramdan’ (Donation of

Labour) given by a group of farmers/beneficiaries/labourers shall be evaluated as “Own

Means” of financing on the basis of the following criteria:

— There should be a provision in the approved “Cost Plan”;

— Actual number of farmers/labourers worked in a project;

— Actual number of days/hours worked;

— Category of farmers/labourers worked i.e. skilled, semi-skilled and unskilled;

— Nature of work done;

— Rate per day/hour keeping in view the provisions of Minimum Wages Act prevalent in the

States;

— Piece rate/volume of work done and payments made for normally such services rendered;

— Certificate from each farmer/Iabourer regarding “Shramdan” given for a project; and

— Estimated and actual measurement of work done before and after the completion of the

assigned job.

2.56 Donation of materials (Like Bricks/Cement/Badarpur/Sand/Stones/Bamboos) , Seeds, Fertilizers

etc..: Donation of materials, seeds, fertilizers etc. can be accounted for as “Own Means” of

financing in the books on the basis of the following guidelines:

— Materials, seeds, fertilizers etc. should form part of the approved “Cost Plan”;

— Nature of materials (seeds, fertilizers etc.) received;

— Actual quantity received and used in the project;

— Standard usage per Sq. feet/cubic feet/acre/hectare as per PWD or other standards;

— Market price of such materials/seeds, fertilizers etc.; and

— Acknowledgement from the donor.

2.57 Free Use of “Capital Equipments”: In case of free use of capital equipments for a specific

purpose/period, the value of the same can be ascertained as “Own Means” on the following

basis:

— Name ofCapital Equipment (e.g. tractor, jeep etc.);

— Number of days/hours used;

— Cost for running and maintenance of capital equipment in the form of:

— Salary

— Repairs and Maintenance

— Other direct expenses, if any

— Depreciation

or

— Equivalent hire charges if the equipment would have been taken on hire.

11

COST PLAN

Item Structure of a Building Project

In Foreign Currency

1

2

Value of Site

.... M2....at (Currency) per M2

Preparation of Site

(Clearing, levelling, demolition, access etc.)

3 Buildings

4

5

6

....M2....at (Currency) per M2

(Cost of each building to be given separately indicating area, type of

construction, rate per M2)

Equipments

(A separate list of equipment and furnishings proposed for the

building is required)

External Works

—Water supply, surface and soil drainage, electricity supply

— Fencing. Landscaping, retaining walls, roads, footpaths, yards.

paved area

Professional Fees

—Architect

—Structural Engineer

—Supervision

—Other consultants

— Local Authorities Charges

— Prints and copying

—Auditor

7

Sub-total Ito 6

8

Contingencies

9

TOTAL 1 to 8

12

In National Currency

COST PLAN

Item Structure of Establishment of Village Industries and Training Centre

Schedules of Budgeted Costs

(Basis of calculation 3 years)

Establishment of Village Industries

4 processing centres (including working capital)

6 raw material depots (including working capital

1.3 3 rural marketing & artisan service centres (including working capital)

1.4 6 sen ice and spare parts workshops (working capital for tools, spare parts,

sundries)

1.5 Starting capital for village industries (margin money/fixed deposit to bank, initial

capital for revolving funds)

1.6 Teechnical information publicity centre

1.7 Mobile industries exhibition

1.8 Managerial help to artisans co-operatives (honoraria to experts, travelling

expenses, other expenses)

In Foreign

Currency

In National

Currency

2.00.000

1.00.000

75.000

8.00.000

4.00.000

3.00.000

60.000

2.40.000

2.00.000

35.000

1.05.000

8.00.000

1.40.000

4.20.000

50.000

2.00.000

8.25.000

33.00.000

1.0

1.1

1.2

Total— 1

13

In Foreign

Currency

In National

Currency

2.0 Training

2.1 Village industries oriented training

2.1.1 Construction and equipment of 5 training centres

of approx. DM 7000 each

35,000

1,40.000

2.1.2 Other training expenses for 600-700 persons (teaching material,

honoraria for teachers/instructors, living expenses for trainees, etc.)

1.05.000

4,20,000

2.2 Industry oriented Training:

2.2.1 Construction and equipment of 3 training centres of approx.

DM 25.000—each

75.000

3.00.000

2.2.2 Other training expenses for 800-900 trainees (teaching material,

living expenses etc.)

46.400

1.85,600

2.2.3 Allowances to 9 trainees/instructors a DM 1.800 p.a.

48.600

1,94.400

3.10.000

12.40.000

1.52.500

6,10,000

Total —2

3.0

Reserve

4.0

Administrative Expenses for Programme Co-ordination

4.1

Administration and office Expenses

40.000

1.60.000

Salaries to 10 staff members of central promotional unit

62.500

2.50.000

1.02.500

4.10.000

13.90.000

55.60.000

4.2

Total — 4

5.

Grand Total (14-24-34-4)

14

Cost Plan

— Programme Activities Budget

Programme

Project:

Description

Year-wise

Total Budget

‘A’ Capital Costs

Total ‘A’

‘B’ Programme Costs

Total ‘B’

‘C’ Office Costs

Total ‘C’

‘D’ Reserves

Total ‘D’

‘E’ Total Cost

(A+B+C+D)

In National

Currency

In

F.C.

Break-up

2nd Year

1st Year

In

F.C.

Budget

Period

In National

Currency

In

F.C.

3rd Year

In National

Currency

In

F.C.

In National

Currency

Cost Plan

— Administrative Expenses Budget for

Programme Co-ordination

Programme

Description

Year-wise Break-up

Total Budget

In

In National

F.C.

Currency

1st

Year

2nd

Year

3rd

Year

In

In National

In

F.C.

In National

In

F.C.

In National

Currency

F.C.

Currency

i) Staff Salary & Benefits

(details attached)

ii) Rent, Rates & Taxes

iii) Water & Electricity Charges

iv) Printing and Stationery

v) Communications

vi) News Papers & Periodicals

vii) Travel & Conveyance

viii) Repairs & Maintenance

ix) Operating cost of vehicles

x) Office up-keep

xi) Office Tea & Tiffin

xii) Conferences. Meeting & Seminars

xiii) Depreciation

xiv) Other Expenses (to specify)

TOTAL

Budget

Period

Currency

Programme

Cost Plan

—Programme Activities Budget

Details of Staff Salary and Benefits

Project

Description

Total Budget

In

Year-wise Break-up

In National

1st

Year

In

F.C.

In National

Currency

F.C.

Sub-Total ‘A’

vii) Contribution to P.F.

viii) Contribution to Gratuity and

Other Funds

ix) Medical Facilities

x) ETC

Sub-Total ‘B?

‘C’ Total

(A+B)

2nd

Year

In

In National

F.C.

Currency

i) Pay

ii) Dearness Allowance

iii) Addl. Dearness Allowance

iv) Housing Allowance

v) Citv Compensatory Allowance

vi) Other Allowances (to specify)

Budget

Period

3rd

Year

In

In National

Currency

F.C.

Currency

Finance Plan

—Source of Funds

Programme

Project:

Description

‘B’ Contribution by ProjectPartner^________________

— In Cash

co

— In non-cash Inputs:

— Donation of land

— Donation of Building

— Donation of Capital Equipments

— Donation of Labour

— Donation of Materials

— Donation of Other Services

TOTAL ‘B’

‘C’ Miscellaneous Income

TOTAL ‘C’

‘D’ TOTAL SOURCES OF FUNDS

(A + B + C)

Year-wise Break-up

Total Budget

In

F.C

‘A’ Contribution by Funding

Agency/Agencies_______

— Remittances

— Debit Notes

— Interests

TOTAL ‘A’

Budget

Period:

In National

Currency

In

F.C.

1st Year

In National

Currency

In

F.C

2nd Year

In National

Currency

In

F.C.

3rd Year

In National

Currency

MANUAL OF FINANCIAL MANAGEMENT

AND

LEGAL REGULATIONS

Ill

PROJECT/PROGRAMME IMPLEMENTATION AND

TRANSFER OF FUNDS BY

FUNDING AGENCIES

CHAPTER III

Programme Implementation And Transfer Of Funds By Funding Agencies

Pages

Introduction

Agreement

The Implementation Plan

The Determination of Demand for Funds

Transfer of Funds

Payment of Subsequent Instalments

Utilisation of Funds

Utilisation of Project Assets

Right of withdrawal and Restrictions

19

19

19

20

20

23

24

24

24

— in para 6. actual cash and bank balances position of project account as on the date of

submission of‘Request for Transfer of Funds’ should be given;

— in para 8, the break-up of estimated payments to be made according to the main budget

items during the period of next three months should be given which in turn should tally

with the figures shown in para 3.3;

3.20 If funds are required for financing cost item shown under the head “Reserves”, the

project-partner should state clearly the nature of expenses and amount involved.

3.21 The information contained in Form No. 1 enables the funding agency to respond to project

partner’s request for transfer of funds as quickly as possible. It is, therefore, suggested that Form

1S?O. 1 should invariably be used by the project partner for requesting transfer of funds. The

funding agency will inform the project-partner in writing when the bank transfer has been

made. If possible, photo copy of bank confirmation of the transfer of funds shall also be sent by

the funding agency directly to the project-partner.

3.22 As and when intimation for the receipt of funds from the funding agency is received by the

project-partner either by means of a letter or bank credit advice through their banker, an entry

for the same should be recorded on the receipt side ofcash book by debit to the respective bank

account and credit to Funding Agency Grant Account. Bank charge, if any. incurred on the

transaction in local currency shall be recorded on the payment side of the cash book by debit to

Reserves Account—Bank Charges and credit to Bank Account.

3.23 ‘Acknowledgement of Receipt’ (in form 2) given on page No. 198

should be signed and

sent to the funding agency by the authorised representative of the project-partner indicating

date of credit of funds in bank account, amount of funds received in National Currency (Bank

advice to be enclosed), amount of funds in foreign currency remitted according to the funding

agency’s advice of payment dated---------------- . The amount received in National Currency

should be included in the next financial statement to be submitted by the project-partner to the

funding agency.

3.24 Request for Transfer of Funds (Form No. 1) and Acknowledgement of Receipt (Form No.

2), during the implementation period of the project, should only be signed by the authorised

representatives of the project-partner for the purpose of dealing with the funding agency. Such

authorisation, including subsequent changes (if any), is generally the responsibility of the

controlling board etc. acting in accordance with the project-partners’ constitution. Prompt

notification of such authorisation including subsequent changes will help the funding agency to

avoid possible delays in payments.

3.25 Bank charges (including cable charges) incurred on the receipt of funds from the funding

agency shall be grouped under cost item “Reserves” in the cost plan and accordingly shown in

the financial statement.

3.26 Interest earned on funds provided by the funding agency and kept in a separate deposit/

savings account with a bank is to be credited to the Funding Agency Account or is to be paid

back. This shall be accounted for on the basis of bank advice received and entered on the

Receipt side of Cash Book. For valid reasons, however, interest may also be utilised for

additional expenditure on the project provided the funding agency has approved it in writing.

3.27 The above, however, does not apply to interest earned on “Revolving funds” which has

been explained in detail separately.

21

3.28 When payment of the approved funds is made by the funding agency and received by the

project-partner, exchange control regulations including Foreign Contribution (Regulations)

Act, 1976 should be observed.

3.29 The funding agency may make direct payments for the purchase of capital items or

supplies etc. supplied under deemed export scheme to third parties on behalf of the project

partner. Such payments shall be made to the suppliers directly by the funding agency after

appraising conformity of ordered goods and cost plan of the project. The funding agency will

notify to the project-partner, the payments made on their behalf, by sending debit notes in the

prescribed form given on page No. 211 to them. The debit note will indicate date of invoice,

name of supplier, details of expenditure, amount in foreign currency, the rate of exchange used,

amount in national currency, allocation in schedule of budgeted costs.

3.30 On the basis of receipt of debit note, the project-partner shall verify the same with the

receipt of capital items/supplies. In case of shortages/damages etc., the project-partner shall

lodge claims with the underwriters/carriers/insurance companies and in addition shall notify

the funding agency of such instances.

3.31 The purchase of capital items shall simultaneously be entered in the Fixed Assets Register

which has been explained in detail separately.

Payment of Subsequent Instalments

3.32 Request for payment of subsequent instalments shall be made by the project-partner to

the funding agency if:

— written confirmation of receipt of all preceding payments has been sent by the project

partner and received by the funding agency;

— all due interim reports (financial as well as narrative) have been received by the funding

agency; and

— project costs are due to be financed from the grant.

3.33 Funds for amounts chargeable against the cost item, “Reserves” of the Schedule of

budgeted costs shall be transferred by the funding agency upon special request by the project

partner stating the amount and nature of such expenses.

3.34 If contrary to expectations, funds received from funding agencies either in full or in part

are not likely to be utilised for due payments within 5 months after receipt, the project-partner

should inform the funding agency accordingly. It can be arranged on mutual understanding to

transfer the corresponding funds to another funding agency assisted project by credit to the

project partner’s account.

3.35 If the project-partner receives contributions from other sources to finance the same project

or programme, he shall inform the funding agency immediately so as to adjust the budget

accordingly on mutual understanding.

3.36 The funding agency may retain 5% of the approved funds on the completion of each

project pending acceptance of the final financial statement and final reports to be submitted by

the project-partner. The intention is to avoid over payments and possible difficulties that may

arise in connection with bank charges, exchange losses, and exchange control in case of

23

refunding over-payments and any interest earned on them. In appropriate cases, exceptions

can be agreed upon by the funding agency and the project-partner.

Utilisation of Funds (As practised by EZE)

3.37The project funds are to be spent only for the purposes specified in the letter of approval and

the budget. Within the scope of the objectives and measures agreed upon, the project-partner is

free to develope the project to achieve the best possible results. To be able to achieve this, the

project partner can exceed the individual budget items by upto 30% to the debit of other items

whereby the budget as a whole remains binding.

3.38 Changes in the project objectives or measures agreed upon, or exceeding the various items

of the estimated expenditure by more than 30% are to be settled between the partner and the

funding agency on mutual understanding. The funding agency will react promptly if any

alterations are proposed.

3.39 Project funds will be utilised efficiently and economically. Orders for larger acquisitions

(i.e. cars, pumps, hospital equipments), buildings and other services will be placed with the

most economic and reliable offerer after having previously compared other tenders.

3.40 If the intended purpose of funding cannot be achieved, the funding agency will be

informed immediately by the project-partner.

Utilisation of Project Assets (As practised by EZE)

3.41 Assets acquired with project funds (e.g. land, buildings, equipments, machinery, furni

ture, vehicles etc.) are the property of the project-partner and will be utilised for the purposes

agreed upon. The same will apply to revolving and disposition funds.

3.42 Funding agency’s prior consent in writing will be secured if the partner feels that assets

cannot be utilised any more for the original purpose. Such prior consent will be required also for

mortgaging or selling the assets or using already created revolving fund for another purpose or

closing it.

3.43 If without funding agency’s prior consent, assets are not utilised any more for the purposes

for which they were originally intended, the project-partner will pay to funding agency

compensation in proportion. The basis for the compensation will be the market value for assets,

and the residual value for funds. Funding agency’s share will be in the same proportion in which

the actual payments have been financed by the funding agencies.

3.44 In the case of an in-voluntary dispossession, for instance expropriation or any other

deprivation of use, a corresponding share of the grant (see para 3.43) will be re-imbursed to the

funding agency, provided that a compensation is received by the project-partner.

Right of Withdrawal and Restrictions

3.45 The project partner can also after the commencement of the project withdraw from the

agreement if circumstances beyond his control hinder a successful accomplishment of the

24

project. A new arrangement will be reached on the use of funds already paid or investments of

funds already made.

3.46 Funds transferred by the funding agency which are

;

not required for funding the project or

programme shall be paid back to the funding agency.

3.47 The funding agency can revoke the funding of the project/programme, stop payments and

reclaim payments already made if:

— the statements or any other information that are the basis for funding are found incomplete

or incorrect;

— the funds are not used according to the terms of the agreement;

— funds transferred by the funding agencies are not matched by the project-partner in the

agreed proportion of funding;

— over-payments have been made;

— the duties of maintaining proper books of account, reporting and other relevant informa

tion to the project are not fulfilled.

3.48 Furthermore, funding agency»may demand payment of interest of 6% per annum from the

date of compensation.

25

MANUAL OF FINANCIAL MANAGEMENT

AND

LEGAL REGULATIONS

IV

BOOK KEEPING SYSTEM

CHAPTER IV

Book-keeping System

Page

A—GENERAL FEATURES OF BOOK-KEEPING SYSTEM

Introduction

Accoounting Concepts

Capital and Revenue

Vouchers

26

27

28

28

B— ESTABLISHING THE BOOK-KEEPING SYSTEM

Bank Account

Books of Account

Subsidiary Records/Registers for Control Purposes

Depreciation

Trial Balance

Bank Reconciliation

Receipt and Payment Account

Income and Expenditure Account

Balance Sheet

Chart of Accounts

Chart of Accounts (Codes)

30

30

34

39

40

40

42

42

42

43

46

Forms

9

A

Cash/Bank Voucher

Journal Voucher

Cash Book

Receipt Book

Cheques/Drafts Receipt Register

Petty Cash Book

Journal Book

Ledger

Attendence Register

Salaries and Wages Register

Muster Roll Form

Agricultural Input Register

Stationery Stock Register

Agricultural Produce Register—Milk

Agricultural Produce Register—Other Products

Fixed Asset Register

Foreign Contribution (Articles) Register

Foreign Contribution (Securities) Register

Telephone and Trunk Call Register

Vehicle’s History Card

Bank Reconciliation Statement

Receipt and Payment Account

Income and Expenditure Account

Balance Sheet

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

70

71

72

73

74

75

76

77

IV Book-Keeping System

A.

General Features of Book-Keeping System

Introduction

4.01 Book-keeping is the system of recording, classifying and summarising all monetary

transactions so that the financial position of an organisation can be ascertained.

4.02 There are two systems of recording transactions namely:

— Single Entry System

— Double Entry System

4.03 Single Entry System: Under this system, the two fold aspect of each transaction as con

sidered in the double entry system is ignored. The essential characteristic of this system is the

keeping of Personal Accounts only; that is, no Real or Nominal Accounts find a place in the

books of account. Such a book-keeping method is incomplete and unsatisfactory because a trial

balance cannot ensue from the books.

4.04 Double Entry System: The system of Book-keeping that “every debit has a credit is known

as the Double Entry System. This system seeks to record every transaction in money or money s

worth in its double aspect—the receipt of a benefit by one account and the surrender of a like

benefit by another account, the former entry being to the account of receiving, the latter to the

credit of the account surrendering.

4.05 The three cardinal principles of double entry book-keeping are:

(a) “Debit what comes in. credit what goes out”—Real Accounts i.e. accounts related to

tangible things—cash, furniture, vehicles etc..

(b) “Debit the receiver and credit the giver”—Personal Accounts.

(c) “Debit all expenses or losses, credit all gains or profits”—Nominal Accounts i.e. salaries,

rent, telephone expenses, grant received, interest earned etc..

4.06 Real Accounts represent transactions which deal with material things such as cash, fixed

assets and stock etc..

4.07 Personal Accounts relate to transactions with persons necessitated by “Credit” transac

tions i.e. where goods are sold and services rendered, payment being made at a subsequent date,

or in the case of “Debit” transactions where payment is made at once for the future delivery of

goods or rendering of services. In Personal Accounts, “Debit Receiver: Credit Supplier .

4.08 Nominal Accounts relate to all account heads relating to expenditure/income connected

with the organisation.

26

e

4.09 The aforesaid principles of double entry are explained with the following illustration:

SI. No.

Accounting Entry

(a)

Receipt of Donation in Cash

Cash Account

Debit

(b)

(c)

(d)

(e)

(0

Principle of Double Entry System

To Donation Account...

Debit what comes in (Real Account)

Credit all gains or profit (Nominal)

(Account)

Deposit of Cash into Bank

Bank Account

Debit

To Cash Account

Debit the receiver (Personal Account)

Credit what goes out (Real Account)

Deposit of Grant-in-aid Cheque into Bank

Bank Account

Debit

To Grant Account

Debit the receiver (Personal Account)

Credit all gains or profit (Nominal Account)

Receipt of Membership Subscription in Cash

Cash Account

Debit

To Membership Subscription Account

Debit what comes in (Real Account)

Credit all gains or profit (Nominal Account)

Payment against Furniture Purchase

bill by Cheque

Furniture & Fixture Account-Debit

To Bank Account

Debit what comes in (Real Account)

Credit the giver (Personal Account)

Payment of Advance to ‘A’ in cash

‘A’ Advance Account

Debit

Debit the receiver (Personal Account)

Credit what goes out (Real Account)

To Cash

Accounting Concepts

4.10 Accounting is the language of affairs of an organisation. To make the language more

meaningful, the following accounting co'ncepts should be understood:

4.11 The “Money Measurement” Concept: Accounting records only those transactions which can

be expressed in monetary terms.

4.12 The “Entity” Concept: The entity of an organisation is different from the individuals who

operate it. Without such distinction, the affairs of the organisation will be mixed up with the

private affairs of the individuals who manage it.

4.13 The “Cost” Concept: Transactions are to be recorded only at the price paid to acquire

it—that is, at its cost—and that this cost is the basis for all subsequent accounting.

4.14 The “Going Concern” Concept: It is assumed that the organisation will exist for a long time.

Transactions are therefore recorded in such a manner that the benefits likely to accrue in future

from money spent now or the future consequences of events occurring now are also taken into

consideration.

4.15 The “Dual Aspect” Concept: Every transaction entered into by an organisation has two

aspects—every debit should have corresponding credit and every credit should have cor

responding debit.

97

Capital = Assets — Liabilities

Assets = Liabilities + Capital

4.16 The “Realisation” Concept: It is a fundamental rule in accounting that profit is not recog

nised to have been earned till it is realised in cash or a third party has legally become liable to

pay the amount.

4.17 The “Accrual” Concept: Known expenditure/liabilities even though not incurred/paid

should be taken into account.

Capital and Revenue

4.18 Revenue expenditure constitutes a charge against surplus and should be debited to

Income and Expenditure Account, whereas capital expenditure is treated as a capital charge

and is shown on the assets side of the Balance Sheet of an organisation. The classification

between Capital and Revenue is significant since the treatment in books of account depends on

the nature of expenditure.

4.19 There is much divergence of opinion and practice in the classification of expenditure

between Capital and Revenue. However, the following indicia have been laid down as

establishing the fact that the expenditure is capital expenditure:

(a) Any expenditure which is undertaken for the purpose of increasing surplus either

positively by way of increasing earning capacity or negatively by decreasing working

expenditure.

(b) If the expenditure, whether increasing the earning capacity or not, produces an asset

comparitively permanent in character, it is capital expenditure.

4.20 Capital expenditure may therefore, be described as an expenditure resulting in the

increase or acquisition of an asset or increase in the earning capacity of a business. Revenue

expenditure, on the other hand, is an expenditure which is incurred for the maintenance of

earning capacity, including the upkeep of the fixed assets and direct and administrative costs of

running an institution.

4.21 A revenue receipt is a receipt which arises from day to day transactions in an organisation

i.e. membership fee, donations, interest on bank account etc.. On the other hand, a capital

receipt is an amount arising because of the disposal of the properties of the institution or specific

capital grants received to form part of the corpus of the institution or life membership fee

received from members.

4.22 The revenue receipt is reflected in the Income and Expenditure Account of an organisa

tion whereas capital receipt is taken on the “liabilities” side of the Balance Sheet.

4.23 Broadly, revenue income minus revenue expenditure pertaining to a stated period will be

the surplus/deficit for that period.

Vouchers

4.24 Every payment made on behalfof an organisation is supported by a voucher. Vouchers are

the office documents which enable the accountant to pass the necessary entries in the books of

28

account. Vouchers should be accompanied by supporting documents such as cash memos, bills,

invoices etc..

4.25 The objectives of vouchers are:

— to have proper evidence of financial transactions

— to establish safe administrative procedures

— to enable proper recording of transactions

4.26 Vouchers give in a summarised manner the serial number and the date of a transaction,

the nature of a transaction, amount in words and figures, analysis within schedule of budgeted

costs i.e. the account head which is debited/credited. the person who has prepared the voucher,

the authority who has passed it for payment/adjustment, the supporting documents such as

bills, invoices, cash memos etc.. Vouchers for payment will also be signed by the recipient in

acknowledgement of receipt of the stated amount in the voucher.

4.27 Vouchers form the basis for passing entries in the original books of account. Vouchers

could be for cash/bank payment, receipts and journal transactions. A proforma of cash/bank

payment voucher and Journal Voucher which are generally used for accounting purposes are

given on page Nos. 53 and 54.

4.28 Vouchers should be prepared and filed separately on day to day basis. Each voucher

should be serially numbered and such number should be mentioned in the respective original

books of account maintained in order to facilitate cross reference. It is advisable to print

vouchers in different colours for the purpose of identification.

4.29 Particular care should be taken in making out vouchers in support of expenditure

representing the project-partner’s own non-cash contribution to ensure that they explain

adequately and iixsuflicient detail the nature and make-up of such expenditure.

4.30 Vouchers whether for cash/bank/journal transactions should be authorised bv a responsi

ble person of the organisation.

4.31 Vouchers should be kept in safe custody of the responsible person in the Accounts

Department.

4.32 Where the book-keeping for the project is kept separate, the relevant vouchers should also

be kept separate.

4.33 Vouchers should normally be kept by the project-partner for 5 years after the funding

agency has approved the last financial statement. However, vouchers are required to be kept for

eight years as per the provisions of Income Tax Act 1961.

29

B.

Establishing The Book-keeping System

Bank Account

4.34 As per agreement between funding agencies and the project-partner, the project-partner

is normally required to open a separate bank account for funds provided by funding agencies.

4.35 Similarly, as per section 13 of the Foreign Contribution (Regulation) Act, 1976 read with

Rule 8 (1) of the Foreign Contribution (Regulation) Rules, 1976 regarding maintenance of

accounts, every association is required to maintain a separate bank account exclusively for

foreign contributions received and utilised.

Books of Account

4.36 Since the project-partner utilises the granted funds self-reliantly, it is necessary to main

tain proper books of account and reporting procedures etc.. The project-partner is required to

keep proper books of account of all receipts and payments of the project or programme in

national currency by following the general principles of book-keeping.

4.37 The books of account should always be maintained in an up-to-date manner.

4.38 The books of account of the project and the corresponding vouchers and other documents

should be kept by the project-partner for 5 years after the funding agency has approved the last

financial statement.

4.39 The following books of account, or equivalent records should normally be kept by the

project-partner:

4.40 Cash Book: It may be recalled that one of the fundamental rules of double entry book

keeping is that all entries must originate from a book oforiginal entry and be posted therefrom to

the ledger. Cash Book is one of the books of original entry. The Cash Book is used for recording

transactions involving the cash/bank receipts and payments in a chronological order. The debit

side (left hand) is used for recording receipts and the credit side (right hand) is for recording

payments.

4.41 The receipt and payment sides normally have cash and bank columns to record cash and

bank transactions. If more than one bank accounts are held by the organisation, either the bank

columns are extended or a separate bank account is opened in the ledger. It may, however, be

kept in mind that bank account which has frequent transactins should be kept in cash book and

the bank account which does not have much transactions should be kept in the ledger.

4.42 The Cash Book should be maintained in the proforma given on page No. 55.

I he

Cash Book should be serially numbered with machine. The project incharge/competent

authority should further certify the page numbers contained in the Cash Book in the beginning

of the Book.

4.43 The Cash Book should be written daily by the Accounts Clerk from the duplicate copies of

receipt book, payment vouchers, cheque book counterfoils etc.. Cash Book should be closed

daily and the closing balance should tally with the actual balance ofcash in safe. Entries in the

Cash Book should also be verified by the project incharge/competent authority at periodical

30

intervals and a note on such verification should be recorded in the Cash Book.

4.44 Entries recorded on the receipt and payment sides of the Cash Book are posted into the

ledger, except “Contra Entries”. “Contra Entries” are adjustments made in the Cash Book

when cash is withdrawn from bank or deposited into the bank. It is denoted by ‘C’ in the Cash

Book.

4.45 Approval of Expenditure: The project-partner will ensure that expenditure is incurred and

payments made only with the approval of the authorised representative(s). This approval will

be evidenced in writing.

4.46 Record of Payments: Every payment made on behalf of the project will be supported by a

voucher indicating reference number, date, amount, description of payment, analysis within

schedule of budgeted costs and signature of the authorised representative(s) together with

relevant external supporting documents.

4.47 All payments whether by cash/cheques/drafts etc. should be “Passed for Payment’ by the

Project Incharge or by a person authorised by him in writing. All payments to outside parties

should preferably be made by cheques. Payments exceeding Rs. 2,500/- should be made by

“crossed cheques only”. In case of payment by cheques, it should be ensured that cheques are

signed by the persons authorised by the Executive Committee/Managing Committee of the

organisation. Before signing the cheques, it should be seen that the relevant details are also

entered in the counter-foils of the cheques. The counter-foils should also be initialled by the

person who has signed the cheques. If a cheque is cancelled, both the foils should be cancelled

and kept in the cheque book.

4.48 Record of Receipts: Receipt of funds from funding agencies should be acknowledged in the

prescribed form, a copy of which will be retained by the project-partner. For all other receipts in

money or money’s worth including cheques/drafts etc., a receipt should be issued. The receipt

book should be kept in the proforma given on page No. 56.

The receipt books should be

printed, serially pre-numbered with machine and prepared in duplicate. The original

perforated receipt should either be handed over to the person from whom the cash/cheque/draft

is received or sent by post. The duplicate copy of receipt should be used as a supporting

document for recording entries in the Cash Book. It should be ensured that receipts are either

signed by the Project Incharge or by a person authorised by him in writing.

4.49 All cheques/drafts/money orders received during a particular day should be entered in

cheques/drafts receipt register and deposited into the bank either on the same day or the next

working day.

4.50 A proforma of cheques/drafts receipt register is given on page No. 57.

Cash receipts

should be entered in the Cash Book on the same day of its receipt whereas cheques/drafts

received should be entered in the Cash Book on the date of deposit into the bank.

4.51 The Project Incharge should also carry out a surprise physical verification of cash at

periodical intervals and a note on such verification should be recorded in Cash Book.

4.52 Petty Cash Book: The Petty Cash Book should be maintained by an organisation where

there are a large number of petty cash transactions of a repetitive nature. In such cases, a Petty

Cash Book in an analytical and columnar fashion is maintained so as not to burden the Cash

31

Book with small and petty cash transactions. A proforma of Petty Cash Book is given on page

No. 58.

4.53 The Petty Cash Book should be serially numbered with machine. The Project Incharge/

Competent Authority should certify the page numbers contained in the Petty Cash Book in the

beginning of the Book. The Petty Cash Book should be written daily by the Accounts Clerk on

the basis of cash payment vouchers.

4.54 Normally, Petty Cash Book is maintained on an “imprest basis” wherein an imprest say

Rs. 500/- is given to the petty cashier for incurring petty expenses on behalf of the organisation.

At regular intervals, the petty cashier submits an account of the expenses incurred alongwith

the supporting documents to the competent authority for verification and sanction for the

reimbursement of the expenses incurred so as to keep the imprest balance at Rs. 500/-.

4.55 The entries recorded in the Petty Cash Book can be taken into the ledger by either of the

following methods:

(a) A petty cash imprest account may be debited with the amounts paid to the petty cashier

in the Cash Book. The total of the petty cash expenses for the month should be debited to

the respective account heads by credit to the petty cash imprest account in the general

ledger by passing a journal entry in the Journal Book. The balance in the petty cash

imprest account in the general ledger would represent petty cash balance in hand.